NEWARK, DE, June 18, 2026 /24-7PressRelease/ — Abstract

The global district cooling market is entering a decade-long expansion phase, projected to climb from USD 36.7 billion in 2026 to USD 77.8 billion by 2036, advancing at a compound annual growth rate of 7.8 percent According Latest Insights by Future Market Insights . This trajectory reflects a structural transition in urban thermal energy infrastructure, where centralized cooling networks are displacing fragmented, building-level air conditioning across residential, commercial, and industrial corridors. Central Cooling Plants retain product leadership with a 42.0 percent share, while Free Cooling captures 52.0 percent of production-technique volume, underscoring a market increasingly defined by energy efficiency and lifecycle economics rather than raw cooling capacity.

Centralized deployment architectures account for 64.0 percent of installed systems in 2026, supported by chilled water plants and large-scale district networks. The United States and South Korea lead regional growth at 7.9 percent and 7.8 percent respectively, propelled by infrastructure modernization, semiconductor-sector demand, and regulatory compliance mandates. Competitive dynamics remain concentrated among ENGIE, Empower, Tabreed, Veolia, and Siemens, each scaling manufacturing and distribution capacity to capture the incremental USD 41.1 billion opportunity emerging through 2036.

Market Dynamics

District cooling has shifted from a niche utility offering into a mainstream infrastructure category as municipalities and large-scale developers reassess the economics of centralized thermal energy distribution. Valued at USD 34.1 billion in 2025, the market is forecast to close 2026 at USD 36.7 billion before compounding to USD 77.8 billion by 2036, representing an incremental opportunity of USD 41.1 billion over the decade. This expansion is not driven by a single demand pole; rather, it reflects converging procurement cycles across residential high-rise development, commercial office and hospitality construction, and industrial process cooling, each contributing recurring specification renewals as legacy end user cooling interfaces reach the end of their operational life.

Read Full Table of Content and after make Decision accordingly for Full Report order: https://www.futuremarketinsights.com/reports/sample/rep-gb-14274

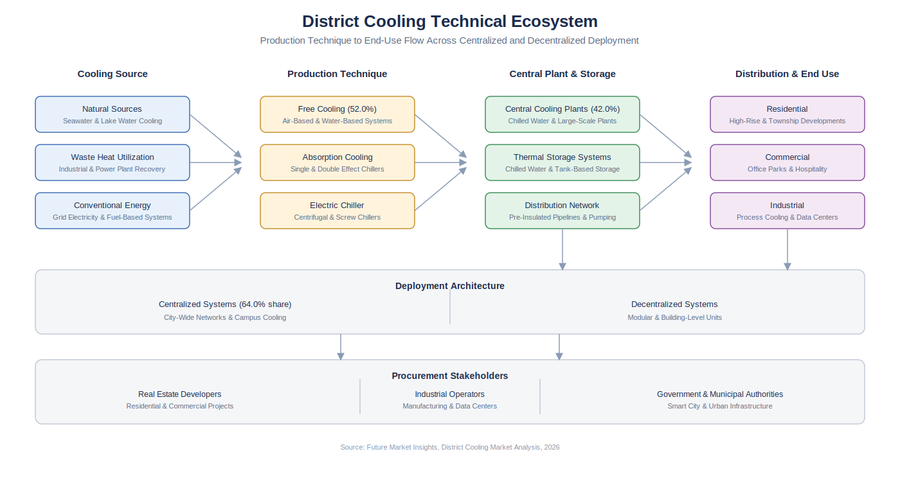

Centralized Systems dominate the deployment landscape, accounting for 64.0 percent of installations in 2026 through city-wide networks, campus cooling architectures, and single-plant systems serving dense urban districts. Within the product hierarchy, Central Cooling Plants lead with a 42.0 percent share, anchored by Chilled Water Plants and Large Scale District Plants that serve concentrated commercial and industrial loads.

Thermal Storage Systems represent the fastest-evolving secondary category, with Chilled Water Storage and Tank Based Storage configurations gaining traction as developers seek to shift cooling loads away from peak-demand electricity pricing windows, a pattern increasingly relevant as grid operators in the United States, South Korea, and the European Union tighten demand-response expectations on large consumers.

Production technique segmentation reveals a clear technological preference: Free Cooling commands 52.0 percent of volume, reflecting buyer appetite for ambient air and water-based cooling methods that reduce reliance on mechanical compression. Absorption Cooling, particularly single and double effect chiller configurations, is gaining share in applications where waste heat recovery from industrial processes or combined heat and power systems creates a low-marginal-cost cooling input. Electric Chiller technology, anchored by centrifugal and screw chiller platforms, continues to serve peak-load and flexible-operation requirements where free cooling or absorption capacity is insufficient, particularly in industrial process cooling and high-density data center applications.

Procurement behavior across real estate developers, industrial operators, and government and municipal authorities is consolidating around suppliers capable of bundling central plant equipment, thermal storage integration, and distribution network components, including pre-insulated pipelines and primary and secondary pumping systems, into a single accountable delivery package. This consolidation favors incumbents with established manufacturing scale and discourages fragmented, single-component vendors, a dynamic that is reshaping competitive positioning across the value chain heading into the 2030s.

Regulatory Drivers

Regulatory architecture is functioning as a primary demand accelerant rather than a peripheral compliance cost across the leading growth corridors. In the United States, Inflation Reduction Act-linked investment incentives are catalyzing aging infrastructure replacement and emission compliance upgrades, positioning the country as the fastest-growing market at 7.9 percent CAGR through 2036. Procurement activity is concentrated in commercial and industrial channels, where specification standards increasingly reference free cooling compatibility and verified performance data as baseline requirements rather than optional differentiators.

The European Union’s regulatory stack, comprising Industrial Emissions Directive compliance, Energiewende-linked infrastructure investment, and CE marking harmonization for central cooling plant equipment, is generating a 7.7 percent growth rate across member states. South Korea’s 7.8 percent expansion is similarly regulation-adjacent, with government research and development support and smart manufacturing investment programs directing capital toward central cooling plants serving the country’s semiconductor, display, and electric vehicle battery manufacturing base.

The United Kingdom’s 7.6 percent trajectory reflects updated building regulations alongside offshore wind infrastructure and Great British Energy program linkages, while Japan’s 7.5 percent growth is shaped by post-Fukushima energy restructuring and JIS quality standard enforcement across aging facility replacement cycles.

Collectively, these frameworks are converging on a common requirement set: verified emissions performance, energy efficiency documentation, and lifecycle total cost of ownership transparency. Suppliers unable to furnish compliance-grade documentation across these dimensions face rising exclusion risk from public-sector and large institutional tenders, a trend research bibliography sources including the International Energy Agency, the U.S. Department of Energy, and the European Commission have each flagged as an intensifying procurement filter through the remainder of the decade.

Technical Ecosystem

District Cooling Technology Ecosystem

Cooling Sources

(Natural Water | Waste Heat | Grid Power)

│

▼

Central Cooling Plants

│

▼

Thermal Storage Systems

(Chilled Water / Ice Storage)

│

▼

Distribution Network Components

(Pipelines, Pumps, Underground Grid)

│

▼

End User Cooling Interfaces

(Heat Exchangers & Smart Controls)

│

▼

Residential | Commercial | Industrial

Applications

The technical architecture of district cooling follows a four-stage value chain beginning with the cooling source. Natural sources such as seawater and lake water, waste heat utilization from industrial and power generation processes, and conventional grid-electricity-fed systems each feed into one of three production techniques: free cooling, absorption cooling, or electric chiller compression.

These techniques in turn supply central cooling plants and thermal storage systems, which interconnect through pre-insulated pipeline networks and pumping infrastructure before reaching residential, commercial, and industrial end users. Deployment architecture splits this delivery between centralized, city-wide networks serving dense urban districts and decentralized, modular building-level systems suited to lower-density or retrofit environments, with procurement ultimately concentrated among real estate developers, industrial operators, and government and municipal authorities overseeing smart city and urban infrastructure programs.

Market Bottlenecks

Despite favorable structural demand, the district cooling market faces meaningful friction in capital-intensive procurement environments. Input cost volatility across steel, copper, and specialized refrigerant components continues to compress margins for manufacturers committed to fixed-price institutional contracts, while capital expenditure constraints among price-sensitive industrial operators slow adoption of thermal storage systems that carry higher upfront costs despite favorable lifecycle economics. Supply chain concentration risk compounds this dynamic, as a relatively small set of manufacturers, including ENGIE, Empower, Tabreed, Veolia, and Siemens, account for a disproportionate share of central cooling plant manufacturing capacity, leaving regional buyers exposed to delivery timeline risk during periods of demand surge.

Competitive pressure from established decentralized alternatives, including high-efficiency split and variable refrigerant flow systems, remains a persistent restraint in markets where district cooling infrastructure has not yet reached critical network density. Real estate developers and industrial operators evaluating total cost of ownership frequently weigh the higher connection costs of joining a district network against the operational simplicity of standalone systems, a calculus that favors district cooling only once a sufficient base of anchor tenants commits to the network, creating a chicken-and-egg dynamic in emerging deployment corridors.

Future Outlook

Looking toward 2036, the district cooling market’s growth will be increasingly shaped by the convergence of thermal storage deployment and data center cooling demand, as cloud providers and colocation operators seek high-density, energy-efficient cooling solutions capable of supporting escalating server loads. This convergence is likely to accelerate adoption of stratified storage and ice-based cooling configurations, particularly in markets such as South Korea and the United States where digital infrastructure investment is compounding alongside traditional residential and commercial buildout.

Strategic positioning among market leaders is expected to center on three priorities: reducing total cost of ownership through free cooling optimization, expanding geographic footprint into high-growth corridors across South Asia and the Middle East, and developing next-generation central cooling plant configurations engineered to meet tightening regulatory and performance benchmarks. Emerging participants, including Keppel DHCS, District Energy St. Paul, ADC Energy Systems, and Emicool, are likely to compete most effectively by specializing in application-specific end user cooling interfaces and underserved regional markets rather than challenging incumbents on manufacturing scale.

Replacement cycles across North America and Western Europe, combined with new network formation in East Asia and the Middle East, position the market for sustained double-digit-adjacent expansion, with the cumulative 2026–2036 opportunity of USD 41.1 billion reflecting both organic capacity growth and the steady displacement of decentralized cooling infrastructure in qualifying urban environments.

District Cooling Market: Key Metrics at a Glance

Market Value (2026) USD 36.7 Billion

Market Forecast (2036) USD 77.8 Billion

Forecast CAGR (2026–2036) 7.8%

Leading Product Segment Central Cooling Plants (42.0%)

Leading Production Technique Free Cooling (52.0%)

Fastest-Growing Market USA (7.9% CAGR)

Regional Growth Comparison (CAGR, 2026–2036)

Country / Region CAGR (2026–2036)

United States 7.9%

South Korea 7.8%

European Union 7.7%

United Kingdom 7.6%

Japan 7.5%

Order Customise Report, share your Details Requirements here: https://www.futuremarketinsights.com/reports/brochure/rep-gb-14274

Conclusion

The district cooling market’s progression from USD 36.7 billion in 2026 to a projected USD 77.8 billion by 2036 reflects a durable realignment of urban thermal infrastructure priorities rather than a cyclical demand spike. Central Cooling Plants and Free Cooling technologies have established clear category leadership, while regulatory frameworks across the United States, South Korea, the European Union, the United Kingdom, and Japan continue to reinforce procurement standards that favor verified efficiency and emissions performance.

As centralized deployment architectures extend further into residential, commercial, and industrial corridors, suppliers capable of integrating central plant equipment, thermal storage, and distribution infrastructure into accountable, lifecycle-priced offerings are positioned to capture the largest share of the decade’s incremental opportunity.

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading global provider of market intelligence, consulting, and syndicated research services, delivering actionable insights across a broad spectrum of industries and technologies. With a strong presence across North America, Europe, Asia Pacific, and the Middle East, FMI helps organizations make informed strategic decisions through data-driven analysis, competitive benchmarking, and forward-looking market forecasts.

—

For the original version of this press release, please visit 24-7PressRelease.com here

Legal Disclaimer: The content on this page is syndicated from independent third-party providers. Kyrion Media makes no warranties or representations regarding the accuracy, completeness, legality, or reliability of the information, including text, images, videos, or licenses. If you are affiliated with this content or have any complaints, copyright concerns, or requests for removal, please contact us at retract@kyrionmedia.com with the specific URL of the content in question. We will review and address valid requests promptly.